Estate Planning Seminar!

October 17, 2019

We invite you to a free seminar on October 17, 2019, at the Ethan Allen Hotel in Danbury, Connecticut (21 Lake Avenue Ext).

We invite you to a free seminar on October 17, 2019, at the Ethan Allen Hotel in Danbury, Connecticut (21 Lake Avenue Ext).

Topic: How Resilient is Your Estate Plan?

The presentation will start at 6:30 PM.

To register, call 203-744-1929 (please provide your email address) or email us at dvv@danburylaw.com. You also can register here: Seminar Registration.

Informative and fun. Come learn and have a great time.

We intend to cover changes of all kinds (not just law and taxes) that will most affect your estate plan.

Reconnect with all the attorneys in our estate planning and probate practice group.

Topics include:

- Probate Courts

- Issues related to Change of Residence

- Coping with the Surge of Conservatorship Proceedings

- How Estate Planning Changes with Each Stage of Life

- Changes in Law that Could Affect Your Estate Plan.

The presentation will start at 6:30 PM. Light refreshments will be served.

To register, click below or call us at 203-744-1929 or email us at

dvv@danburylaw.com.

REGISTER HERE

The Presenters and Their Topics:

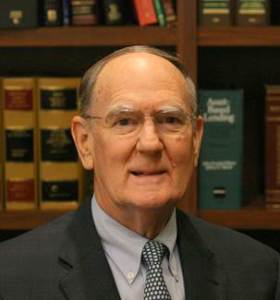

Richard L. Emerson

Richard L. Emerson

Topic: Insights from a Former Probate Judge

The Probate Courts have been affected by important changes. Attorney Richard L. Emerson will inform us about the workings of the Probate Courts as only a former Probate Court Judge can.

Attorney Richard L. Emerson served as the Probate Judge in Redding, Connecticut, for over thirty years. His legal practice concentrates on estate administration, probate, estate planning, trust and estate disputes and general corporate representation. He also has mediated contested probate matters and has appeared as an expert witness for other attorneys.

James J. Flaherty, Jr.

James J. Flaherty, Jr.

Topic: Thinking About Moving Out of Connecticut? Consider

This.

We often hear about people moving out of Connecticut. Is this merely a case of “the grass is always greener…”? James J. Flaherty, Jr., will discuss issues related to a change of residence. Whether you stay or go, if you are wondering about leaving, this is information you need.

Attorney James J. Flaherty, Jr., practices from the firm’s Southbury office and is a member of the estate planning and probate group. Jim’s practice focuses on assisting high net worth individuals, including closely held business owners, in the creation of wealth succession plans. In addition to estate planning, Jim works with individuals on Medicaid (Title 19) and asset protection planning.

Alyson R. Marcucio

Alyson R. Marcucio

Topic: Coping with the Surge in Conservatorship

Proceedings

The increasing number of conservatorship proceedings creates additional demands on our Probate Courts. Alyson R. Marcucio will discuss planning steps to work around crowded court dockets and long wait times.

Attorney Alyson Marcucio is a member of the firm’s estate planning and probate group, with an emphasis on elder law and

planning for those who have chronic disabilities. Alyson’s practice includes long term care, incapacity and special needs planning, eligibility for Medicaid and other public benefits, and conservatorship proceedings.

Elizabeth J. Hartery

Elizabeth J. Hartery

Topic: Estate Planning for Each of Life’s Stages

Life is often thought of as having twelve stages. Estate planning starts with the sixth stage and ends with the twelfth: late adolescence; early adulthood; midlife; mature adulthood; late adulthood; and death and dying. Liz Hartery will discuss how the planning focus changes as we pass through each stage.

Attorney Elizabeth J. Hartery is an associate in the firm’s estate planning and probate group, assisting with estate planning, estate settlement, probate matters, and elder law issues.

Richard S. Land

Richard S. Land

Master of Ceremonies

Attorney Richard S. Land heads up the firm’s estate planning and probate group, helping individuals from all walks of life to manage and dispose of their assets in an orderly fashion through lifetime transfers and through transfers at death by wills and trusts.

Richard has authored and produced dozens of educational videos on estate planning and trust and estates topics, authored several computer generated estate planning document assembly systems and authored an online estate plan review program.

No Admission Charge

Our seminars are always strictly educational and well attended. Space is limited so please let us know if you plan to attend.

Light snacks, desserts and beverages will be offered.

To register, click on this link: Seminar Registration.

Please join us at the Ethan Allen Hotel (21 Lake Avenue Ext., Danbury, CT) on October 17, 2019.

We look forward to seeing you.

Chipman Mazzucco Emerson LLC

Attorneys at Law

44 Old Ridgebury Road

Suite 320

Danbury, CT 06810

203-744-1929

![185775_1745456110853_1072275011_31952001_6630745_n[1]](https://cmlplaw.me/wp-content/uploads/2011/11/185775_1745456110853_1072275011_31952001_6630745_n1.jpg)

In Part I (

In Part I (