Have you heard scary claims that, if you do not have a Living Trust or avoid probate, probate costs and fees may take 50% of your estate? Maybe you weren’t fooled but you may have been confused. We would like to help clear up the confusion.

Part 3 also covers the fees of Executors and Attorneys and the purpose of a probate accounting. When is an accounting necessary? What information should be included in the account? And, why should your Executor prepare an account?

Part 1 covers the probate process, the probate application, preparation of the inventory, and common issues an Executor should be aware of.

Part 2 covers significant legal issues, tax reporting and payment obligations.

Part 3, partly described above, caps off the presentation with a discussion of accounting duties, probate expenses and common problems faced by an Executor.

Part 3 also covers the fees of Executors and Attorneys and the purpose of a probate accounting. When is an accounting necessary? What information should be included in the account? And, why should your Executor prepare an account?

If you have questions about estate settlement and other related matters including Wills, trusts and estate planning, please contact us. We are here to help.

Trust law in Connecticut was changed recently so we updated our Trusts and Trust Administration Video.

If you are named as a Trustee in the Will of a relative or friend, there are a number of duties, and related traps, you need to be aware of. Your responsibilities will be many. It’s easy to get overwhelmed or miss something important. Watch the video below to learn about the duties of a Trustee and common problems Trustees face.

Help others find our informative videos. If you find this video helpful,please “like” it and share it with your friends.

An update of our video on Estate Settlement is in the works. Stay tuned. If you subscribe here: YouTube channel, you’ll be notified as soon as it’s posted.

If you are a trustee who has been struggling to manage a trust, or if you have any basic questions, please contact us. We are here to help.

Estate plans are so much more than just a Will. Tim and Liz have a light-hearted discussion covering a number of estate planning options and techniques including living trusts, living wills, how to deal with difficult family issues, and what people need to know about pet trusts.

Subscribe to the Ounce of Prevention podcast. In each episode, Tim will focus on a specific legal issue and how it could impact your everyday life.

The goal of the podcast is to educate and inspire our listeners to harness the law to make life just a little bit easier.

For more information about topics mentioned in the podcast, contact Tim Herring at 203-744-1929 x19 or tmh@danburylaw.com. Visit our website at https://www.danburylaw.com/ to learn more.

The Chipman Mazzucco Emerson attorneys and staff would like to thank all of the Health Care Providers and First Responders who are working on the frontlines during the COVID-19 Pandemic.

Frontline Estate Plan Package

Just as you are helping all of us, we would like to help you. A link at the end of the video will bring you to information about our special Frontline Estate Planning Package offered at a well-deserved savings for health care providers and first responders. We sincerely hope that you will forward this within your organizations or to anyone close to you on the frontlines.

Does the pandemic have you worried about whether your existing estate plan works for you now?

Or maybe you are simply using the enforced quarantine time to catch up on important things that you keep putting off.

Either way, Chipman Mazzucco Emerson has an easy way to guide you through what you need to know to make sure your estate plan is updated and meets your current needs.

Our complimentary updated Online Estate Plan Review asks a series of specific questions that will alert you to issues you should address to make certain your plan still works. The latest version of this program covers a number of recent law changes, including:

The Tax Cuts and Job Act of 2017

SECURE Act of 2019

Numerous changes in State and federal estate tax exemptions

You can complete the process in ten to fifteen minutes. When you are finished, you’ll receive a detailed personalized report that identifies issues that require your attention. Here is our new video explaining how the review works and how to register for your personalized report.

To access our complimentary Online Estate Plan Review, please click on the link or image below:

To help you face your estate planning challenges, we have updated our Basic Estate Planning video presentation to cover the Tax Cuts and Jobs Act (effective January 1, 2018) and the SECURE Act (effective January 1, 2020). You can take a look at the video here (Basic Estate Planning After the Tax Cuts and Jobs Act) or below.

Here is a very brief summary of what the videos cover:

Parts 1 and 2: No matter where you live (or die), your estate plan can be destroyed if you don’t know the difference between probate property and non-probate property. We cover this distinction in Part 1. We also cover what a trust is and how a trust can help accomplish certain estate planning goals: protecting assets from the beneficiary’s creditors and risks; asset management for a beneficiary who needs management help; estate tax reduction; and more. We acknowledge that the unfortunate Connecticut estate tax exists (and many other states do not have an estate tax) but, in most cases, we can help with effective workarounds. Part 2 covers Connecticut and federal estate taxes (also New York estate taxes) including how life insurance death benefits are taxed for estate tax purposes.

Parts 3 and 4: Your Will can include provisions that reduce or eliminate estate taxes. Parts 3 and 4 describe such Wills. Danger: Existing Wills with old estate tax provisions can have the unintended effect of disinheriting a spouse. We cover how to deal with such a risk. We also cover new rules allowing one spouse to give his or her federal estate tax exemption to the surviving spouse. The surviving spouse’s federal estate tax exemption could be more than $11,580,000. In addition, we cover Will provisions that can protect assets from a beneficiary’s long term care costs.

Parts 5 and 6: Not all trusts that are designed to save estate taxes are the same. Part 5 compares the different types of trusts. As Part 5 ends, we begin a discussion of common estate planning mistakes and Part 6 continues the discussion.

Parts 7 and 8: These parts cover estate tax and income tax planning for retirement accounts such as 401(k) accounts and IRAs.

Part 9 to Part 13: These parts include a complete discussion of revocable living trusts with a comprehensive comparison between a plan that uses a revocable trust and a plan that relies on a Will without making use of a revocable living trust. Part 13 ends with a description of how Connecticut probate court fees are calculated.

Part 14: This part covers the basic gift tax rules and techniques.

Part 15: This is the final part and covers gifts of life insurance policies with brief mention of other advanced gift techniques.

We hope our updated basic estate planning videos help you. If you have questions about any of the estate planning concepts mentioned in the video, please call.

Washington has been salivating over the potential that retirement accounts represent for increasing tax revenues. If only such accounts (IRAs, 401(k) plans, 403(b) plans and similar retirement accounts) could be subjected to tax now….

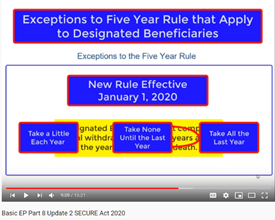

The SECURE Act (effective January 1, 2020) is a step toward increasing taxes on your retirement accounts. Ironically, the acronym SECURE stands for “Setting Every Community Up for Retirement Enhancement.”

On January 20, 2020, we posted an update of Part 8 of our Basic Estate Planning Video Series (called Basic Estate Planning after TCJA). In updated Part 8 we cover the new rules under the SECURE Act that affect your estate planning. Please click here,or on the video link below, to watch Part 8 (15 minutes).

Help others find our informative videos. If you find the video helpful, please “like” it and share it with your friends.

In theory, the most significant new rule appears simple: with limited exceptions, most inherited retirement accounts must be withdrawn within ten calendar years after the year in which the account owner passes away. The simplicity of this change masks the complexity of the calculations that may be needed when you are making estate planning decisions regarding your retirement accounts.

If you know the new rules, you will begin to understand why it may make sense

to consider converting to Roth IRAs before you pass away;

for a surviving spouse to consider converting part of the spouse’s regular or rollover IRA to a Roth IRA;

to consider leaving some of your IRA directly to your children instead of to your surviving spouse while also leaving a large part of your IRA to your surviving spouse;

in some cases, for the beneficiary to take no distributions from the IRA until the tenth year after the owner’s death and in other cases to take much earlier distributions; and

in some cases to use trusts as beneficiaries of retirement accounts when, in the past, you would have been more inclined to name individuals.

The conclusion is the same as always. More complexity means more need to consult with your accountants and financial advisers (and maybe with your lawyers).

We hope these materials add to your understanding. Please let us know if you have questions.

The Probate Courts have been affected by important changes. Attorney Richard L. Emerson will inform us about the workings of the Probate Courts as only a former Probate Court Judge can.

Attorney Richard L. Emerson served as the Probate Judge in Redding, Connecticut, for over thirty years. His legal practice concentrates on estate administration, probate, estate planning, trust and estate disputes and general corporate representation. He also has mediated contested probate matters and has appeared as an expert witness for other attorneys.

Topic: Thinking About Moving Out of Connecticut? Consider This.

We often hear about people moving out of Connecticut. Is this merely a case of “the grass is always greener…”? James J. Flaherty, Jr., will discuss issues related to a change of residence. Whether you stay or go, if you are wondering about leaving, this is information you need.

Attorney James J. Flaherty, Jr., practices from the firm’s Southbury office and is a member of the estate planning and probate group. Jim’s practice focuses on assisting high net worth individuals, including closely held business owners, in the creation of wealth succession plans. In addition to estate planning, Jim works with individuals on Medicaid (Title 19) and asset protection planning.

Topic: Coping with the Surge in Conservatorship Proceedings

The increasing number of conservatorship proceedings creates additional demands on our Probate Courts. Alyson R. Marcucio will discuss planning steps to work around crowded court dockets and long wait times.

Attorney Alyson Marcucio is a member of the firm’s estate planning and probate group, with an emphasis on elder law and

planning for those who have chronic disabilities. Alyson’s practice includes long term care, incapacity and special needs planning, eligibility for Medicaid and other public benefits, and conservatorship proceedings.

Life is often thought of as having twelve stages. Estate planning starts with the sixth stage and ends with the twelfth: late adolescence; early adulthood; midlife; mature adulthood; late adulthood; and death and dying. Liz Hartery will discuss how the planning focus changes as we pass through each stage.

Attorney Elizabeth J. Hartery is an associate in the firm’s estate planning and probate group, assisting with estate planning, estate settlement, probate matters, and elder law issues.

Attorney Richard S. Land heads up the firm’s estate planning and probate group, helping individuals from all walks of life to manage and dispose of their assets in an orderly fashion through lifetime transfers and through transfers at death by wills and trusts.

Richard has authored and produced dozens of educational videos on estate planning and trust and estates topics, authored several computer generated estate planning document assembly systems and authored an online estate plan review program.

No Admission Charge

Our seminars are always strictly educational and well attended. Space is limited so please let us know if you plan to attend.

Light snacks, desserts and beverages will be offered.

On January 18, 2019, final regulations and a special notice were published regarding the 20% income tax deduction related to certain pass through income.

Trade or Business?

The Notice (Notice 2019-07) offers owners of rental real estate an opportunity to benefit from significant deductions related to rental income. This blog discusses the content of the Notice.

As an appendix to previously posted videos on the pass through income deduction, we posted a video regarding the Notice:

This blog is to discuss the Notice 2019-07 in more detail.

It’s not always easy to determine whether your rental real estate activity satisfies the somewhat vague definition of a trade or business so the IRS tried to provide a bright line test (call it a “safe harbor”) for determining whether the deduction will be available to you for the rental income you receive.

The safe harbor is described in Notice 2019-07 in the form of a Proposed Revenue Procedure. If your rental activity income satisfies the criteria described in the Notice, you can be confident that your rental activity income will qualify for the 20% pass through income deduction under section 199A of the Internal Revenue Code.

The safer harbor provisions apply only to Rental Real Estate Enterprises. A Rental Real Estate Enterprise is an interest, or multiple interests, in real estate held directly by an individual or Relevant Pass Through Entity (aka “RPE” such as a limited liability company, S corporation or partnership), for the production of rents but the definition excludes triple net leases and interests used to any extent as a personal residence. Commercial and residential real estate cannot be part of the same Rental Real Estate Enterprise.

For purposes of the 20% deduction that applies to pass through income under Section 199A of the IRC, your Rental Real Estate Enterprise will be deemed a trade or business if certain requirements described in the Notice are satisfied. Keep in mind that only certain income of a trade or business can qualify for the deduction so this is a key point for income earned through your rental activities.

The Notice says that your rental activity will be treated as a trade or business if (i) you maintain separate books and records for each rental real estate enterprise; (ii) you or your agents devote 250 or more hours per year to rental services with respect to the rental real estate enterprise; and (iii) you keep contemporaneous records related to the rental services.

The records must include: (i) the hours performed, (ii) a description of the services performed, (iii) dates on which the services were performed, and (iv) who performed the services.

The requirement that the records must be contemporaneous has been waived for 2018 so, if you do not have good records for 2018, you can try to do the best you can to reconstruct how you performed rental services in 2018.

Some things you do will count as rental services and some things will not. The Notice includes a specific list of activities that count as rental services. Here is the list:

Advertising to rent or lease property;

Negotiating and executing leases;

Verifying information in the applications of prospective tenants;

Daily operations, maintenance and repairs;

Management of real estate;

Purchasing materials; and

Supervision of employees and independent contractors.

Keep in mind that you will get credit for the time put in by your employees, agents and independent contractors so, if you have others doing the work for you, you should insist that they keep contemporaneous records of the work they do.

Also keep in mind that some of the time devoted to your rental activity will not count as rental services. The time you or your agents spend traveling from property to property will not count. Also, time devoted to financial and investment management relating to your real estate rental activities will not count. Accordingly, the time you spend arranging financing, acquiring property, studying or reviewing financial statements or reports regarding your properties, or planning, managing, or constructing long term capital improvements will not count.

To claim the benefits of the safe harbor, you must file a statement indicating that all the requirements of the Notice have been satisfied. The statement must be signed by the taxpayer or authorized representative and include the following:

“Under penalties of perjury, I (we) declare that I (we) have examined the statement, and, to the best of my (our) knowledge and belief, the statement contains all the relevant facts relating to the revenue procedure, and such facts are true, correct, and complete.”

We are currently working on Section 2 of Part 3 of our video which will cover:

Planning to avoid the phase-out zone;

Additional planning to maximize pass-through income deductions based on wages and capital expenditures;

How transferring business interests to family members and trusts can create additional pass through income deductions; and

How converting pass through income to wages can increase pass through deductions.

We frequently post articles relating to estate planning, estate settlement and elder law issues to this blog. We also post notices about our client seminars here. When we do, we send out notices to clients and friends of the firm. If you would like to get our notices, please join our mailing list by clicking below.

We recently posted to YouTube the video of our annual fall estate planning seminar (held on October 25, 2018). Here is a playlist containing all three segments: Basic Estate Planning and Elder Law in a Nutshell.

Basic Estate Planning and Elder Law in a Nutshell

In Video 1 (Estate Planning for Beginners), Elizabeth J. Hartery covers the basics of Wills, revocable trusts, powers of attorney, conservatorships and health care directives including living wills. Approximately 30 minutes.

In Video 3 (Elder Law in a Nutshell), Alyson Marcucio covers the practice of elder law as part of the continuum of planning for the welfare of the family. In the case of elder law, this means counselling and representing seniors and the disabled as well as their representatives (such as conservators, trustees and agents under a power of attorney) and family members regarding a range of issues including health and personal care, legal capacity, public benefits, special needs, insurance, housing options and more. Approximately 24 minutes.

![185775_1745456110853_1072275011_31952001_6630745_n[1]](https://cmlplaw.me/wp-content/uploads/2011/11/185775_1745456110853_1072275011_31952001_6630745_n1.jpg)

Join Email List

Join Email List