Trust law in Connecticut was changed recently so we updated our Trusts and Trust Administration Video.

If you are named as a Trustee in the Will of a relative or friend, there are a number of duties, and related traps, you need to be aware of. Your responsibilities will be many. It’s easy to get overwhelmed or miss something important. Watch the video below to learn about the duties of a Trustee and common problems Trustees face.

Help others find our informative videos. If you find this video helpful,please “like” it and share it with your friends.

An update of our video on Estate Settlement is in the works. Stay tuned. If you subscribe here: YouTube channel, you’ll be notified as soon as it’s posted.

If you are a trustee who has been struggling to manage a trust, or if you have any basic questions, please contact us. We are here to help.

Estate plans are so much more than just a Will. Tim and Liz have a light-hearted discussion covering a number of estate planning options and techniques including living trusts, living wills, how to deal with difficult family issues, and what people need to know about pet trusts.

Subscribe to the Ounce of Prevention podcast. In each episode, Tim will focus on a specific legal issue and how it could impact your everyday life.

The goal of the podcast is to educate and inspire our listeners to harness the law to make life just a little bit easier.

For more information about topics mentioned in the podcast, contact Tim Herring at 203-744-1929 x19 or tmh@danburylaw.com. Visit our website at https://www.danburylaw.com/ to learn more.

Does the pandemic have you worried about whether your existing estate plan works for you now?

Or maybe you are simply using the enforced quarantine time to catch up on important things that you keep putting off.

Either way, Chipman Mazzucco Emerson has an easy way to guide you through what you need to know to make sure your estate plan is updated and meets your current needs.

Our complimentary updated Online Estate Plan Review asks a series of specific questions that will alert you to issues you should address to make certain your plan still works. The latest version of this program covers a number of recent law changes, including:

The Tax Cuts and Job Act of 2017

SECURE Act of 2019

Numerous changes in State and federal estate tax exemptions

You can complete the process in ten to fifteen minutes. When you are finished, you’ll receive a detailed personalized report that identifies issues that require your attention. Here is our new video explaining how the review works and how to register for your personalized report.

To access our complimentary Online Estate Plan Review, please click on the link or image below:

Effective July 1, 2015, Connecticut Probate Court fees have been increased.

As the chart below indicates, fees for a decedent’s estate with a value of $2,000,000 or less are unchanged. Fees for an estate with a value more than $2,000,000 are increased significantly without any cap. The fee that applies to the excess over $2,000,000 is 0.5% up from 0.025%.

Before the increase, the fee was capped at $12,500 (the fee that applied to an estate with a value of $4,754,000). If the estate was larger than $4,754,000, the fee would remain at $12,500. Accordingly, under the old fee schedule, the fee for an estate having a value of $50,000,000 would be $12,500. Under the new fee schedule, the fee for an estate having a value of $50,000,000 would be increased to $245,615.

In general, the value of the estate is the value determined for estate tax purposes with some adjustments for property that passes to a spouse (in that case only one-half is included).

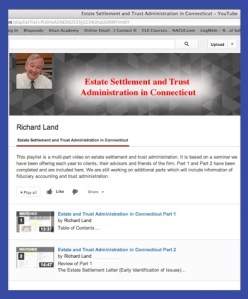

The trust administration portions (Parts 4, 5 and 6) of our video/slideshow presentation on Estate Settlement and Trust Administration in Connecticut have been completed and posted to YouTube.

The videos cover trust administration including a Trustee’s duties, risks that Trustees face, applicable rules and regulations, common problems Trustees face, and Trustee compensation.

You can view Parts 4, 5 and 6 here:

Estate and Trust Administration Part 4 (Trusts): What is a trust? What is trust administration? What are the rules that apply to trust administration? What does a Trustee do? What risks are Trustees exposed to? What are the Trustee’s duties?

Estate and Trust Administration Part 5 (Trusts): Part 5 covers common problems faced by trustees while administering a trust including issues relating to accounting, investments and self-dealing.

Estate and Trust Administration Part 6 (Trusts): Part 6 (the final Part) continues coverage of common problems faced by trustees while administering a trust including potential claims related to contracts that a trustee makes while administering a trust, claims based on a trustee’s negligence and other torts, claims based on environmental contamination of trust real property, and claims related to improper payments and distributions. This Part also includes a brief discussion on Trustee compensation.

To view the complete video starting with Part 1 click on the image below:

We hope you find our Estate Settlement and Trust Administration videos informative.

Notice: To comply with U.S. Treasury Department rules and regulations, we inform you that any U.S. federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction, tax strategy or other activity.

We frequently post articles relating to estate planning, estate settlement and elder law issues to this blog. We also post notices about our client seminars here. When we do, we send out notices to clients and friends of the firm. If you would like to get our notices, please join our mailing list by clicking below.

New Video Part 3: Estate Settlement and Trust Administration in Connecticut

Part 3 of our video/slideshow presentation on Estate Settlement and Trust Administration in Connecticut has been posted to YouTube.

The video covers judicial accounting requirements, including new rules of practice effective July 1, 2013, Probate Court fees, fees of Executors and Administrators, and attorney fees.

You can view Part 3 (9 minutes) here:

Additional parts will be posted in the future dealing with important principles of trust administration.

For Parts 1 and 2, go directly to the YouTube Playlist by clicking on the image below:

We hope you find our Estate Settlement videos informative. Stayed tuned for the rest of the videos in the series.

Notice: To comply with U.S. Treasury Department rules and regulations, we inform you that any U.S. federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction, tax strategy or other activity.

We frequently post articles relating to estate planning, estate settlement and elder law issues to this blog. We also post notices about our client seminars here. When we do, we send out notices to clients and friends of the firm. If you would like to get our notices, please join our mailing list by clicking below.

New Video: Estate Settlement and Trust Administration in Connecticut

Parts One and Two of our video/slideshow presentation on Estate Settlement and Trust Administration in Connecticut have been posted to YouTube. They discuss estate settlement up to preparation of the final account.

Additional parts will be posted in the future dealing with fiduciary accounting, expenses involved in estate settlement and trust administration, and important principles of trust administration.

Go directly to the YouTube Playlist. Click on the image below:

You can view Part I separately (13 minutes) here:

Connecticut Estate and Trust Administration Part 1

You can view Part 2 separately (15 minutes) here:

Connecticut Estate and Trust Administration Part 2

We hope you find our Estate Settlement video informative. Stayed tuned for the rest of the videos in the series.

Notice: To comply with U.S. Treasury Department rules and regulations, we inform you that any U.S. federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction, tax strategy or other activity.

We frequently post articles relating to estate planning, estate settlement and elder law issues to this blog. We also post notices about our client seminars here. When we do, we send out notices to clients and friends of the firm. If you would like to get our notices, please join our mailing list by clicking below.

The American Taxpayer Relief Act of 2012 (“ATRA” effective January 1, 2013) will change everything about estate tax planning. We recently updated our Basic Estate Planning Video to reflect ATRA and posted it to YouTube.

Background

April 30, 2013 (Updated April 20, 2015)

We offer seminars to our clients, their advisors, and other friends of the firm, every year. One of the most popular has been our Basic Estate Planning Seminar. On March 14, 2013, we offered our Basic Estate Planning seminar at the Maron Hotel, Danbury, Connecticut. The seminar covered the topics mentioned below.

Those who could not attend the seminar may be interested in taking a look at the Basic Estate Planning video that we recently finished updating to reflect the recently enacted American Taxpayer Relief Act of 2012 (effective January 1, 2013).

The presentation is in 15 parts. Click on the red “Basic Estate Planning after ATRA (15 Parts)”heading below and then click “Play All” under “Basic Estate Planning” at the top of the YouTube page.

Basic Estate Planning after ATRA (15 Parts)

We describe each of the parts below with an individual link to each one.

Part 1: Introduction. Wills and probate property vs. nonprobate property.

Part 2: Beneficiaries, mistakes with nonprobate property, trust basics, guardian appointments, life insurance beneficiary designations, and estate taxes.

Part 3: Wills, the estate taxation of life insurance death benefits, tax issues and asset protection issues relating to Wills, and disclaimer Wills.

Part 4: Formula marital deduction Wills, exemption trusts, risk of disinheriting the surviving spouse as estate tax exemptions increase, the portable estate tax exemption, and asset protection bypass trusts.

Part 5: Formula marital deduction Wills (and exemption trusts) vs. disclaimer Wills (and disclaimer trusts), and common estate planning mistakes.

Part 6: Common estate planning mistakes continued, the duties of an Executor, the duties of the Trustee, the duties of a guardian, planning for post-death cash needs, and the generation skipping tax.

Part 7: Retirement plan accounts (IRAs, 401(k) plans, 403(b) accounts, etc.), estate taxation on retirement plan accounts, the risk of a circular tax on tax problem at death of account owner, life insurance and irrevocable life insurance trusts as a solution.

Part 8: Retirement plan accounts and related income tax issues, effects of beneficiary designations on deferral periods, spouse as beneficiary and tax deferred rollovers, required minimum distributions, and tax treatment of inherited IRAs, and the five year payout rule.

Part 9: Revocable living trusts, the living trust as a Will substitute, probate avoidance, planning for incapacity, and establishing a revocable living trust.

Part 10: Comparison of revocable living trust plan with non-living-trust plan, treatment of lifetime issues, powers of attorney as an alternative to the revocable living trust, and what it means to avoid probate.

Part 11: Comparison continued, avoiding ancillary probate in other states where real property is located, creditors’ claims and safe harbors for the Executor, and income and estate taxes.

Part 12: Comparison (continued), accounting requirements, releases from liability, continuing trusts and continuing probate court jurisdiction, reasons for considering revocable living trusts, management during incapacity, and real property in other jurisdictions.

Part 13: Reasons for considering a revocable living trust (continued), controversial estate plans, probate notice requirements, disruption of support for third parties, probate and related delays, simplifying estate settlement for survivors, nonreasons for considering revocable living trusts, the living trust as tax neutral, and probate court fees.

Part 14: Gift planning, gift and estate tax exemptions, exclusions for small gifts, gifts to education funds (529 plans), exclusions for qualified tuition and medical costs, gift tax marital deductions, gifts to U.S. citizen spouse, and gifts to noncitizen spouse.

Part 15: Gifts of life insurance policies, incidents of ownership, irrevocable trusts as owner, three year rule relating to transfers of life insurance policies, and sophisticated gift techniques (qualified personal residence trusts, grantor retained annuity trusts, valuations for gift tax purposes, gifts to charities and charitable trusts).

Notice: To comply with U.S. Treasury Department rules and regulations, we inform you that any U.S. federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction, tax strategy or other activity.

We frequently post articles relating to estate planning, estate settlement and elder law issues to this blog. We also post notices about our client seminars here. When we do, we send out notices to clients and friends of the firm. If you would like to get our notices, please join our mailing list by clicking below.

The recent American Taxpayer Relief Act (effective 1/1/2013) could have been named the Great American Estate Planning Simplification Act. All but the very wealthy could call January 1, 2013, Federal Estate Tax Liberation Day. In other words, all but the very wealthy will be able to rely on simple Wills (Wills that don’t include complicated tax and trust provisions) unless one of the exceptions listed below applies to you.

Exceptions:

(1) You live in a state that still has an estate tax. Connecticut has an estate tax with an “exemption” of $2,000,000 and New York has an estate tax with an exemption of $1,000,000.

(2) Special problems plague your beneficiaries: creditor problems; divorces and troubled marriages; poor judgment; gambling habits; drug dependence; health problems; special needs; and poor financial training, financial skills or lack of interest in financial matters.

(3) A need to plan for long term care, whether at home or in a nursing home, for a surviving spouse or other beneficiary.

(4) Your primary beneficiary is your current spouse from a second marriage and you want to provide for the children of a previous marriage.

(5) Your children or other beneficiaries are too young to handle an inheritance or have special needs to consider.

(6) You have a business which will require management if it is to provide appropriately for your beneficiaries after your death.

(7) You are concerned about the management of your assets for you and your family in the event of your incapacity.

(8) You want to disinherit an undeserving relative or you would like to include provisions in your planning documents that your survivors might consider controversial.

(9) You have difficult-to-manage assets (for example, a closely held business, rental properties, collections of art, antiques and other creative works, weapons, etc.).

(10) You are concerned that your surviving spouse’s remarriage after your death will result in a diversion of your assets away from your children or other intended beneficiaries.

(11) You may be wealthier (for estate tax purposes) than you think you are. To determine the size of your estate, start by counting everything that will pass to others at the time of your death: home, retirement accounts, annuities, IRAs, life insurance, bank accounts, stocks and bonds—everything. Is it over $5,250,000? If so the Great American Estate Planning Simplification Act probably does not apply to you.

(12) You are in a same-sex or other “nontraditional” committed relationship (married or otherwise).

(13) Your estate is increasing and there is a strong possibility that, as a result of your efforts, luck, inflation, additional life insurance, or a combination of such factors, you will join the ranks of the “very wealthy”. In that case, it may be important for your documents to include all the existing tools for effective “post mortem” tax planning. See: It’s Not Too Late (Fixing Your Estate Plan After Your Death).

(14) You want to provide for your grandchildren by bypassing your children to some extent.

(15) You want to provide benefits for your grandchildren in amounts that may exceed one generation skipping tax exemption (currently $5,250,000).

(16) Although disadvantages of probate are often overstated, you nevertheless wish to arrange your affairs to avoid probate.

(17) Unique facts reveal unique problems that often require unique (and perhaps not simple) solutions.

With the above exceptions (and probably others I have not thought of), a simple Will may be all you need.

For those of you who currently have in place more complicated, tax sensitive documents, it may be very important for you immediately to change to something simpler. If the tax provisions in your Will are based on the federal estate tax exemption, failure to change to a simpler Will may result in unnecessary Connecticut or New York estate tax (more than $250,000 for Connecticut residents and more than $400,000 for New York residents) at the time of your death. For more details, see our companion post on this blog here: “New Risks of Unnecessary State Estate Taxes.”

We frequently post articles relating to estate planning, estate settlement and elder law issues to this blog. We also post notices about our client seminars here. When we do, we send out notices to clients and friends of the firm. If you would like to get our notices, please join our mailing list by clicking below.

Notice: To comply with U.S. Treasury Department rules and regulations, we inform you that any U.S. federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction, tax strategy or other activity.

Many estate planning clients come to us with the same question: “How can my estate avoid probate when I die?” There is a common misconception among members of our community that probate is an arduous process that will deplete estate assets and should be avoided at all costs. However, in many cases, the probate process is not much more time consuming or costly than avoiding probate and can provide certain benefits that are unavailable to estates that avoid probate.

When is Probate Necessary?

The first step in understanding the probate process, and when probate is necessary, is to understand the difference between probate property and non-probate property. Probate property is all property which is owned by a decedent, in his or her sole name, and without beneficiary designations. Non-probate property is all other property owned by a decedent such as joint property, retirement accounts with designated beneficiaries and assets owned by a living trust established by a decedent prior to death.

The following are examples of commonly owned probate property and non-probate property:

Probate Property:

Checking account owned solely by the decedent

Vacation home owned solely by decedent

Life insurance owned by the decedent with no designated beneficiary

Automobile owned solely by the decedent

Non-Probate Property:

Retirement account owned by the decedent payable to the decedent’s surviving spouse

Savings account owned jointly by the decedent and the decedent’s surviving spouse

Life insurance owned by the decedent, payable to the decedent’s surviving spouse as the designated beneficiary

Home owned jointly by the decedent and the decedent’s surviving spouse with rights of survivorship (but if owned jointly as tenants-in-common, the decedent’s half of the home would be probate property)

Assets owned by a living trust established by the decedent

When an individual passes away, it is clear who has the authority to access his or her non-probate property. For example, a joint account owner has access to joint accounts; a designated beneficiary of life insurance has the authority to claim the death benefit; and the Trustee of a living trust has authority to access to the assets owned by the trust. No one must be appointed by the Probate Court to have such authority. If the decedent’s estate includes probate property, on the other hand, no one has the authority to access such property and probate becomes necessary.

The Probate Process

In a nutshell, probate is the process of appointing an Executor (or Administrator, if the decedent did not leave a Will), identifying and collecting a decedent’s property, paying the debts, taxes and expenses of the decedent’s estate, and distributing the remaining property to the beneficiaries of the estate.

If the decedent left a Will, the process begins by proving the legal validity of the Will and asking the Probate Court to appoint the Executor of the estate. If the decedent did not leave a Will, the process begins by asking the Court to appoint an Administrator of the estate. Once appointed, pursuant to Connecticut law, the Executor or Administrator will have the duty to complete the following estate settlement steps:

Identify the decedent’s property (probate property and non-probate property) and determine the date-of-death value of all such property;

Take possession of and safeguard the probate property;

Prepare and file an Inventory of all probate property (with date-of-death values) with the Probate Court;

Prepare and file the decedent’s final income tax returns;

Prepare and file the estate’s income tax returns and the estate tax returns;

Identify and pay the claims of creditors, the expenses of estate administration, and taxes;

Prepare and file a Return of Claims and List of Notified Creditors with the Probate Court;

Prepare and file a Final Account (or, for some estates, a Statement in Lieu of Account) with the Probate Court; and

Distribute the remaining property to the beneficiaries of the estate.

The Final Account is a list of all probate property (starting with the Inventory), all income earned on such property (interest, dividends, etc.), all sales, and all debts and expenses paid from the estate. It also includes a list of assets remaining after all estate obligations have been satisfied and a schedule of proposed distributions of the remaining property to the beneficiaries of the estate.

If the decedent left a Will, the beneficiaries of the estate will be determined according to the terms of the Will. If the decedent did not leave a Will (i.e. the decedent died “intestate”), the beneficiaries of the estate will be the decedent’s heirs-at-law in accordance with State statutes (for information about intestacy laws in Connecticut, see “I don’t need a Will”).

After the Final Account has been approved and distributions made, the Executor (or Administrator) files a Closing Account with the Probate Court and the probate process is complete.

It is worth noting that, although the steps applicable in each state are analogous, the details (due dates, forms, filing and probate court fees, etc.) can vary significantly from state to state.

Probate Avoidance

Probate can be avoided with various estate planning techniques (a subject for another article). For some estates, there may be compelling reasons to avoid probate. You should consult an estate planning attorney to determine whether any such reasons apply to you. In many cases, however, avoiding probate merely means avoiding the obligation to file certain documents with the Probate Court (such as the Inventory and Final Account) and payment of related filing fees.

For example, some people avoid probate by establishing living trusts (revocable trusts) and transferring all of their assets to their trust. If a decedent transferred all of his assets to a living trust prior to his death and his estate included no probate assets, probate would not be necessary (barring complicating factors). Nevertheless, the Trustee of the trust would have an obligation to: (i) identify and take possession of the trust assets (if the Trustee has not already done so), (ii) file income tax and estate tax returns, (iii) identify and pay the debts, taxes and expenses of the decedent’s estate, (iv) prepare an account to present to the beneficiaries of the trust, (v) and distribute trust assets in accordance with the terms of the trust. In this example, even though the estate avoided probate, the Trustee still has most of the same obligations as the Executor’s obligations outlined above.

Keep in mind that avoiding probate does not mean the estate avoids estate taxes. Estate taxes are based on the value of a decedent’s gross estate which includes probate and non-probate property. Connecticut, in particular, requires all estates to prepare and file a Connecticut estate tax return even if the value of the estate is less than the Connecticut estate tax exemption and no Connecticut estate tax would be due.

In addition, avoiding probate does not mean an estate avoids the Probate Court fee. The Probate Court charges a statutory fee, based on the value of a decedent’s gross estate, which is assessed when the estate tax return is filed.

Benefits of Probate

The probate process can provide certain benefits and protections that are unavailable to an estate that avoids probate. As discussed above, in Connecticut the Executor or Administrator has a duty to file an Inventory and Final Account with the Probate Court. The Account should document every penny in and every penny out of the estate. Probate Court supervision provides extra protection to estate beneficiaries in the event an Executor or Administrator attempts to abuse its power.

Probate Court supervision can also benefit the Executors and Administrators. Troublesome beneficiaries will have a more difficult time contesting the actions of an Executor or Administrator if the Probate Court has given its “stamp of approval” on the Final Account of the estate.

In addition, probate court procedure limits the time during which creditors of an estate may make a claim for payment by the Executor or Administrator. When the Executor or Administrator is appointed, the Probate Court publishes notice to creditors notifying them to present their claims to the Executor or Administrator. Creditors have 150 days to present a claim. After that period, if distributions have been made, the Executor or Administrator is free from liability from future creditors. Without probate, the decedent’s estate is subject to the applicable statute of limitations which range from 2 to 6 years (subject to tolling statutes) depending on the nature of the claim.

[This article is meant to provide a basic overview of the probate process in the context of estate settlement, including some of the potential benefits of probate. It is not intended to be a complete analysis of the probate process or the pros and cons of probate and probate avoidance. For questions and detailed legal advice, please contact your attorney.]

We frequently post articles relating to estate planning, estate settlement and elder law issues to this blog. We also post notices about our client seminars here. When we do, we send out notices to clients and friends of the firm. If you would like to get our notices, please join our mailing list by clicking below.

Notice: To comply with U.S. Treasury Department rules and regulations, we inform you that any U.S. federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction, tax strategy or other activity.

![185775_1745456110853_1072275011_31952001_6630745_n[1]](https://cmlplaw.me/wp-content/uploads/2011/11/185775_1745456110853_1072275011_31952001_6630745_n1.jpg)

![185775_1745456110853_1072275011_31952001_6630745_n[1]](https://cmlplaw.me/wp-content/uploads/2011/07/185775_1745456110853_1072275011_31952001_6630745_n1.jpg?w=300) Posted on August 1, 2015

Posted on August 1, 2015

Join Email List

Join Email List