Tax Increases on Retirement Plan Accounts: A Simple Change Adds to Complexity

Washington has been salivating over the potential that retirement accounts represent for increasing tax revenues. If only such accounts (IRAs, 401(k) plans, 403(b) plans and similar retirement accounts) could be subjected to tax now….

The SECURE Act (effective January 1, 2020) is a step toward increasing taxes on your retirement accounts. Ironically, the acronym SECURE stands for “Setting Every Community Up for Retirement Enhancement.”

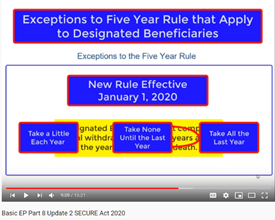

On January 20, 2020, we posted an update of Part 8 of our Basic Estate Planning Video Series (called Basic Estate Planning after TCJA). In updated Part 8 we cover the new rules under the SECURE Act that affect your estate planning. Please click here,or on the video link below, to watch Part 8 (15 minutes).

Help others find our informative videos. If you find the video helpful, please “like” it and share it with your friends.

In theory, the most significant new rule appears simple: with limited exceptions, most inherited retirement accounts must be withdrawn within ten calendar years after the year in which the account owner passes away. The simplicity of this change masks the complexity of the calculations that may be needed when you are making estate planning decisions regarding your retirement accounts.

If you know the new rules, you will begin to understand why it may make sense

- to consider converting to Roth IRAs before you pass away;

- for a surviving spouse to consider converting part of the spouse’s regular or rollover IRA to a Roth IRA;

- to consider leaving some of your IRA directly to your children instead of to your surviving spouse while also leaving a large part of your IRA to your surviving spouse;

- in some cases, for the beneficiary to take no distributions from the IRA until the tenth year after the owner’s death and in other cases to take much earlier distributions; and

- in some cases to use trusts as beneficiaries of retirement accounts when, in the past, you would have been more inclined to name individuals.

The conclusion is the same as always. More complexity means more need to consult with your accountants and financial advisers (and maybe with your lawyers).

We hope these materials add to your understanding. Please let us know if you have questions.

![185775_1745456110853_1072275011_31952001_6630745_n[1]](https://cmlplaw.me/wp-content/uploads/2011/11/185775_1745456110853_1072275011_31952001_6630745_n1.jpg)

Posted by Richard S. Land, Attorney, Chipman Mazzucco Emerson LLC, Attorneys at Law, Danbury, CT, 06810, 203-744-1929 x29, rsl@danburylaw.com.

Explore posts in the same categories: Estate Tax and Estate Planning DevelopmentsTags: 401(k), 403(b), estate planning, income tax, IRA, retirement, roth, SECURE Act, trust

You can comment below, or link to this permanent URL from your own site.

Leave a comment